Entikis is a leading provider of bookkeeping and financial services that help businesses and individuals “trade chaos for clarity”. We turn intricate financial duties into well-structured, useful reports. From daily bookkeeping to strategic planning, our knowledgeable staff takes care of everything to keep your finances accurate and prepared for an audit. As one review notes, clients value our professionalism and personalized advice.We take the time to learn about your needs and update you at every stage.

Our Services

At Entikis, we offer end-to-end financial management solutions tailored to your unique goals:

Business Intelligence & Analytics: Using personalised dashboards and reports, we transform unstructured data into strategic insights. You may find opportunities and make decisions with confidence thanks to our analytics. We use this insight to help your organisation succeed, as research indicates that data-driven projects can lower costs and increase productivity.

Digital Integration & Automation: Entikis leverages cutting-edge digital solutions (cloud accounting, secure portals, AI) to streamline your workflows. For example, 94% of firms now use cloud-based accounting for efficiency. We implement tools like QuickBooks Online and AI-driven reconciliation to automate routine tasks, optimize cash flow and budgets, and enable real-time reporting.

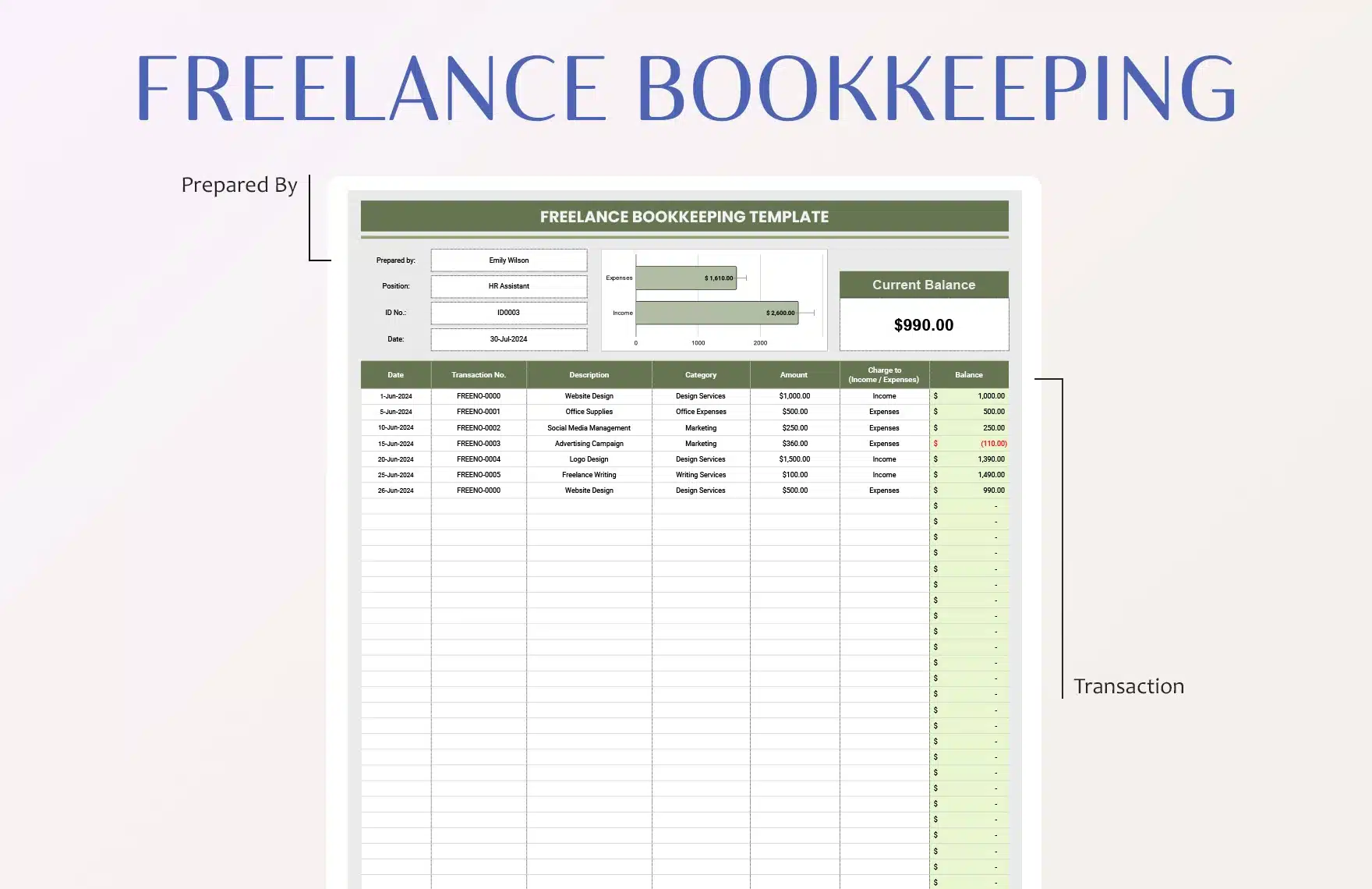

Bookkeeping & Accounting: We maintain accurate ledgers and perform timely reconciliations to ensure your books accurately reflect the true state of your business. Outsourcing finance tasks to experts like Entikis “allows you to trade chaos for clarity” and frees your team to focus on growth.

Outsourced CFO & Advisory: Get CFO experience on a part-time basis without paying for full-time services. We offer cash-flow management, forecasting, budgeting, ROI analysis, and strategic financial planning. This adaptable, results-oriented strategy lowers overhead while providing you with excellent financial advice.

Tax Compliance & Audit Support: Our staff is highly skilled in both audit preparation and tax regulations. We reduce risk and make sure you’re always prepared for an audit or tax filing by keeping your documents current and compliant.